In the first part of this series attempting to sum up the issues facing UK science and innovation policy, I tried to set the context by laying out the wider challenges the UK government faces, asking what problems we need our science and innovation system to contribute to solving.

In the second part of the series, I posed some of the big questions about how the UK’s science and innovation system works, considering how R&D intensive the UK economy should be, the balance between basic and applied research, and the geographical distribution of R&D.

In the third part, I discussed the institutional landscape of R&D in the UK, looking at where R&D gets done in the UK.

In the fourth part, looking at the funding system, I considered who pays for R&D, and how decisions are made about what R&D to do.

In the fifth part, I looked in more detail at UK Research and Innovation, the government’s main agency for funding academic science.

In the sixth part, I looked at the other routes that the UK government funds R&D, particularly through government departments.

In this, the final section of my survey of the routes by which the UK government funds R&D, I turn to two areas with the most uncertainty. The first of these is the future of the UK’s participation in the EU Horizon programme. I’ll discuss the distinctive roles of EU funding, and what might replace it in the increasingly likely scenario that the UK is not able to associate. The second is the new agency the Advanced Research and Invention Agency, set up by Act of Parliament in early 2022, and currently just establishing itself; here I’ll suggest some early thoughts about the role this might play in the overall system.

7.1. Horizon Europe – past participation and future prospects of association

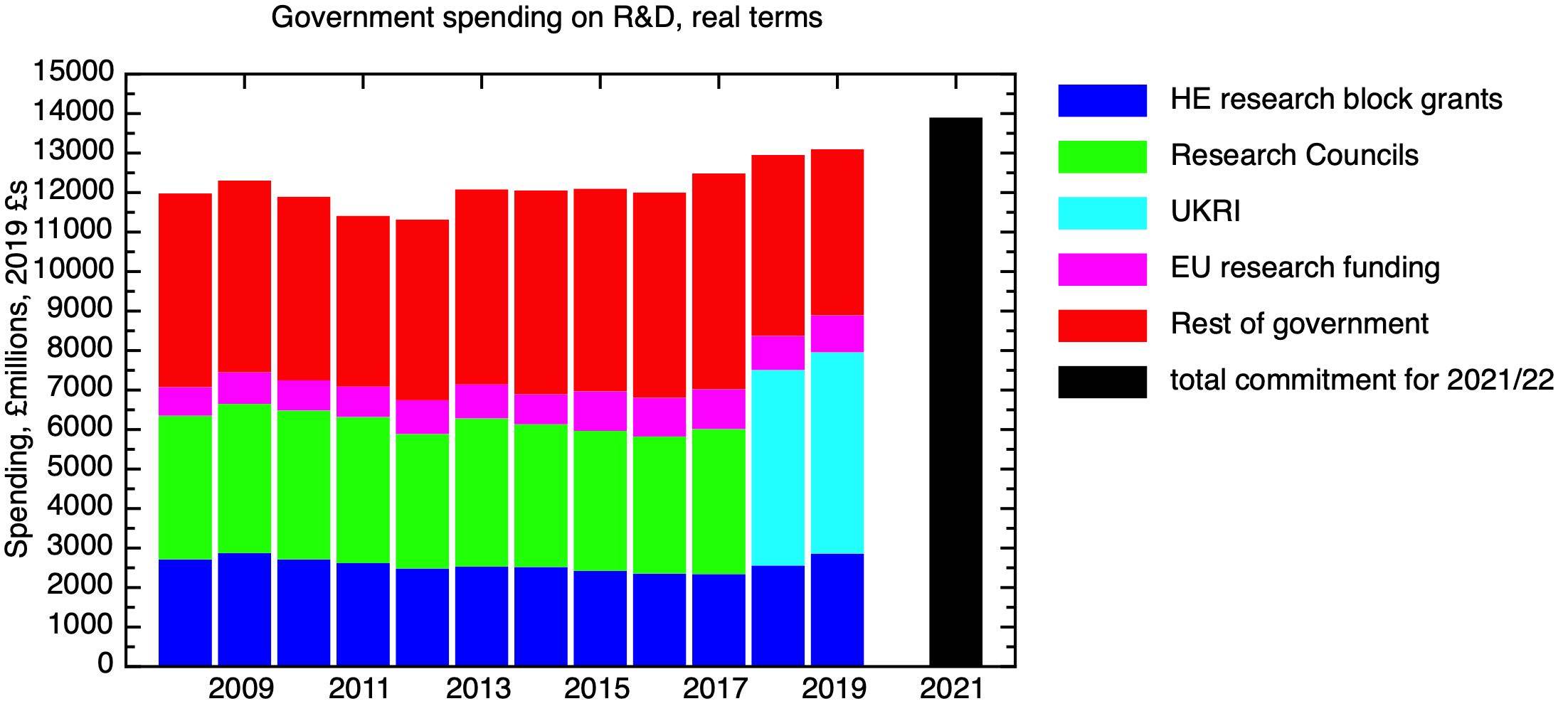

In the past, the UK government has funded R&D indirectly through the EU Horizon programme, which provided research grants to UK researchers in HE and to UK businesses, often as part of larger collaborative programmes with researchers and businesses from elsewhere in Europe. EU research funding to UK universities and businesses has been on a very material scale; of course ultimately this money came from the UK’s contributions to the overall budget. In the UK’s national accounts, this was accounted for by a notional cost that reached a high point of £1.46 billion in 2019.

Because EU research money was allocated competitively, there wasn’t a direct relationship between the money the UK put into the budget and the research money the UK received. In fact, because of the UK’s relative research strength, the UK got back significantly more money than it put in. According to an analysis of the 2007-2013 cycle, the UK’s indicative contribution to the budget was €5.4 bn, but it received €8.8 bn of funding for research, development and innovation.

After the UK decided to leave the EU, a consensus developed that the UK should seek to stay associated with the EU’s R&D programmes, an option already taken up by other non-member states such as Switzerland, Norway and Israel. The Trade and Cooperation Agreement between the EU and the UK contained a draft protocol establishing the UK’s association with Horizon Europe (with the exception of the European Innovation Council). “The Parties affirm that the draft protocols set out below have been agreed in principle and will be submitted to the Specialised Committee on Participation in Union Programmes for discussion and adoption. The United Kingdom and European Union reserve their right to reconsider participation in the programmes, activities and services listed in Protocols [I and II] before they are adopted since the legal instruments governing the Union programmes and activities may be subject to change. The draft protocols may also need to be amended to ensure their compliance with these instruments as adopted.”

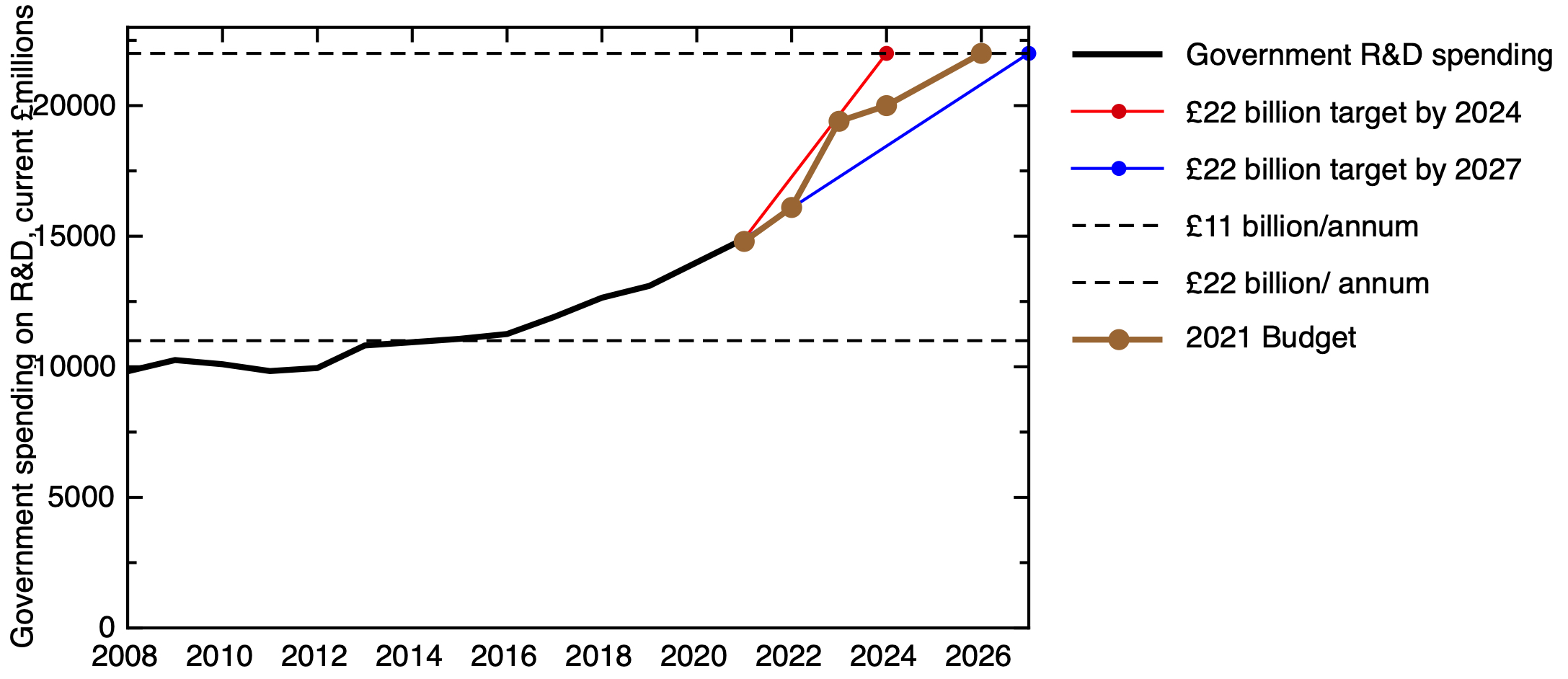

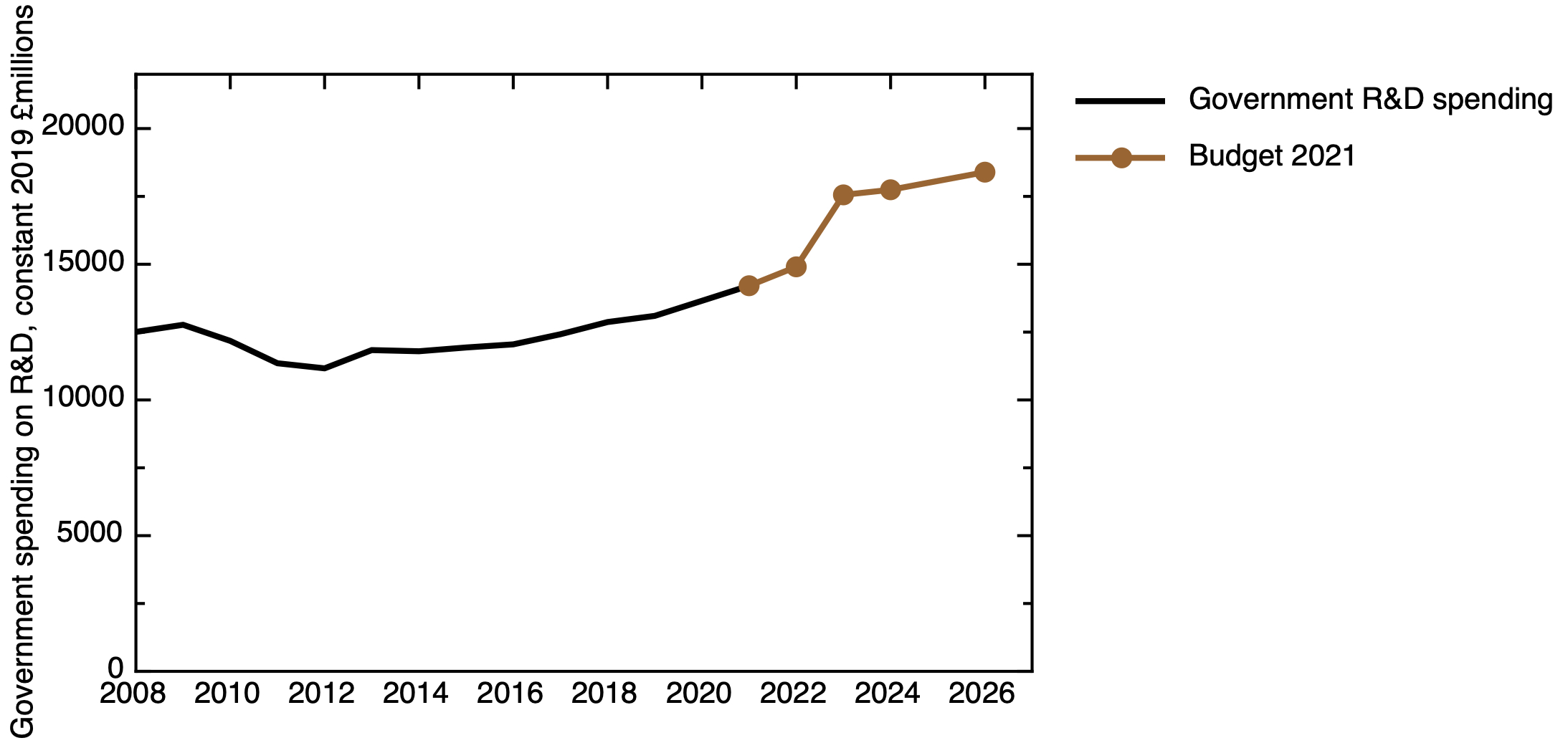

If the UK does associate, it will need to contribute financially to the Horizon Europe programme. In contrast to the situation when the UK was a member state, when it received more back from EU R&D programmes than it notionally contributed, as an associated country it would need to cover not only the full cost of R&D activities funded in the UK through Horizon UK, but also a substantial additional overhead. The money for this was set aside in the 2021 Comprehensive Spending Review; it amounted to £1.3 bn in 21/22, rising to £2.1bn 24/25.

As I write, the draft protocol has not yet been finalised by the EU side, and given the wider political situation, it seems increasingly unlikely that it will be finalised any time soon. The UK government made a commitment at the time of the 2021 CSR that, in the event of the UK not associating, the money set aside would be retained in the science budget, redeployed in a set of programmes that reproduced the benefits of EU association – the so-called “Plan B”.

On July 20th, the government released more details of “Plan B”, restating the commitment to use the Horizon money for alternative science programmes. “In the event we are unable to associate, we will use the funding allocated to Horizon Europe at the 2021 Spending Review to build on our existing R&D programmes with flagship new domestic and international research and innovation investments to support top talent, drive end-to-end innovation and foster international collaboration with EU and global partners.”

7.2. The Three Pillars of Horizon Europe

The EU’s R&D programmes are agreed for seven year cycles; the current cycle – Horizon Europe – assigns €95.5 billion for the period from 2021-27. The overall goals of the programme are specified in terms of the strategic goals of the European Union – tackling climate change, meeting the UN’s Sustainable Development Goals, and boosting the EU’s competitiveness and economic growth.

To support these broad goals, Horizon Europe supports three “Pillars”. The first of these is “Excellent Science”. This includes the European Research Council, together with schemes supporting early career researchers and collaborative research and training for PhD students. The European Research Council supports investigator led basic science and humanities research; this has a very high reputation in the scientific community, for reasons I’ll discuss below. However, it is important to remember that it is a relatively small part of the overall Horizon programme – it’s been allocated €16 bn in the current cycle.

The second pillar is for “Global Challenges and European Industrial Competitiveness”, which supports research collaborations built around sectors, challenges and missions. These typically involve both academic and industrial researchers in multinational collaborations.

The third pillar is new to the current cycle – “Innovative Europe” is focused on developing more high tech start-up companies, with a new “European Innovation Council”, a “European Institute of Innovation and Technology”, and support for regional innovation ecosystems. In the event of association, the UK will opt out of the “EIC accelerator” – that part of pillar 3 which provides investment funding to companies.

Underpinning the whole programme is an aspiration to create a “European Research Area”, with free and easy movement of people and research groups across the continent, lubricated by exchange schemes for scientists (particularly at early career stages) and cross-border transferability of grants. In the past the UK has benefitted from this, with a scientific and institutional infrastructure that has made the country an attractive destination for scientists from other European countries.

7.3. Why scientists love the European Research Council

Amongst elite scientists in the UK, the main driving force for an enthusiasm for the UK to associate with Horizon Europe is to be able to continue to participate in the European Research Council. This, in part, simply reflects how successful the UK has been in winning competitive funding through this route. For example, in the competition for the most established researchers – the Advanced Grants, which provide €2.5 million over 5 years for a single investigator and their team – UK based researchers won 22% of all grants between 2008 and 2020, compared to 16% and 12% to the two next most successful nations, Germany and France respectively (source).

But beyond the self-interest of UK scientists, why is the European Research Council so highly thought of? It has a clarity of purpose, with a single-minded focus on investigator driven basic research, with no predetermined priorities, but with an emphasis on supporting high risk/high gain proposals. It is correctly perceived as highly competitive, attracting proposals from the most outstanding researchers across Europe – currently its grantees have won nine Nobel prizes. Its decisions are made by a peer review process which is widely considered to be fair, rigorous and well executed.

Peer review isn’t easy to do well. In section 2 of this series, in discussing a possible world-wide slow-down in scientific productivity, I mentioned the suggestion that peer review can lead to conservatism and can suppress radical new ideas. In section 5, I suggested that there was a lack of confidence in the scientific community in the credibility of the peer review systems that the UK Research Councils run. In the light of these concerns, it’s worth asking what the European Research Council gets right about peer review (while recognising that even the ERC’s process is probably not perfect, for example in tricky areas like handling highly interdisciplinary proposals).

In my opinion, there’s nothing magic about the ERC’s approach to peer review. The process involves committees of experts (and, to declare a personal interest, I recently served on the expert panel for Advanced Grants in my own field of Condensed Matter Physics). Those panels invite written comments on proposals from worldwide specialists they choose for their appropriateness to judge individual proposals. In a final meeting, the panels consider the referees’ reports, with interviews with the proposers to give them the chance to respond to criticisms, and come to a collective judgement about which proposals to give highest priority for funding.

What makes this work? The starting point must be high quality panels, with a good range of expertise, the ability to take a broad view, and an effective chair. At its best, the ERC has developed a virtuous circle, in which the high quality of the proposals means that outstanding scientists are prepared to put the time in to serve on panels, while in turn it is the credibility of the process that attracts applications from the best scientists from across a whole continent. It is the researchers on the panels who select the remote referees, using their knowledge of the field to select the most appropriate ones, and then applying their own critical scientific judgement to resolve any discrepancies and differences of opinion between referees. Sufficient time is set aside for in-depth decisions – a single proposal round will involve two panel meetings, each of which can take up to a week.

Meanwhile administrative support is provided by high quality subject specialists working full-time for ERC as programme managers. In the UK, the research councils were forced to make serious cuts on their office staff in the early 2010s, because it was mistakenly believed that these subject specialists represented an administrative overhead, rather than being a precondition for the most effective allocation of R&D funding. This mistake should not be repeated (and, indeed, should be corrected).

7.4. “Plan B” for non-association

The “Plan B” document published this July (Supporting UK R&D and collaborative research beyond European programmes) usefully sets out some principles for how the money set aside for association with Horizon Europe will be used in the event that association doesn’t materialise. But details of implementation remain sketchy, and delivery may prove challenging to the existing agencies and bodies that will be charged with executing these schemes.

These agencies are mostly in UKRI, with a particularly important role for Innovate UK, with the National Academies potentially playing a role in the “talent” schemes. These are largely fellowships at various career stages, that will be in part fill some of the role of the European Research Council, though without the benefits of the institutional strength that ERC has developed, as outlined in the last section.

The emphasis of measures taken so far has been on stabilising the system, in particular keeping in the UK outstanding scientists who have been awarded ERC grants, but who can’t take them up without moving to an EU member state. The commitment has been made to guarantee the funding of any Horizon UK grant awarded to UK based researchers for the lifetime of the grant. It is going to be important to ensure that this happens without bureaucratic hurdles, in perception or reality, as HE institutions in the EU will be making energetic efforts to recruit these researchers.

The last point emphasises the importance of making sure the UK remains an attractive destination for overseas scientists, and promoting researcher mobility to make sure that the UK is centrally integrated in international networks of expertise. The plan here remains vague, but states the intention to fund “bottom-up collaborations with researchers in partner countries around the globe; multilateral and bilateral collaborations; and Third Country Participation in Horizon Europe”.

Measures for supporting business R&D will be funnelled through Innovate UK; it seems these will largely build on existing schemes. The aim is to support both domestic and international collaborations. The international dimension will be particularly important in supporting high technology SMEs to participate in trans-national supply chains and innovation systems, many of which, of course, involve EU member states.

The local and regional dimension of support for innovation systems is also important. EU funding – including structural funding as well as direct R&D funding – has been important in developing clusters in economically lagging parts of the UK, such as Northern England, Wales and Northern Ireland. The Shared Prosperity Fund is likely to offer only a partial substitute for EU structural funds, so it is encouraging to see a commitment to drive “the development of emerging clusters throughout the UK”, and the statement that the “Plan B” portfolio “will support our mission of levelling up the UK and build on our commitment to increase domestic R&D investment outside of the Greater Southeast by at least a third over the spending review period and at least 40% by 2030.”

Moving forward with the association of the UK with Horizon Europe would seem to require a breakthrough in wider EU/UK relations that currently doesn’t seem very likely. In the absence of such a breakthrough, the priority needs to be for the new administration to confirm the funding of plan B, and move very quickly to turn what are currently rather high level plans into deliverable programmes.

7.5 The Advanced Research and Invention Agency (ARIA)

The most recent addition to the UK’s R&D funding landscape is the new funding agency, the Advanced Research and Invention Agency. This was established by an Act of Parliament, finalised in early 2022. It was a personal priority of the Prime Minister’s former chief advisor, Dominic Cummings, who emphasised the need to have a funding agency with the freedom to take big risks, modelled loosely on the US agency ARPA. ARPA was set up in the late 1950’s to ensure technological supremacy for the US armed forces, and research it supported has underpinned world-changing technological innovations such as the internet, the satellite location system that GPS evolved from, and stealth aircraft.

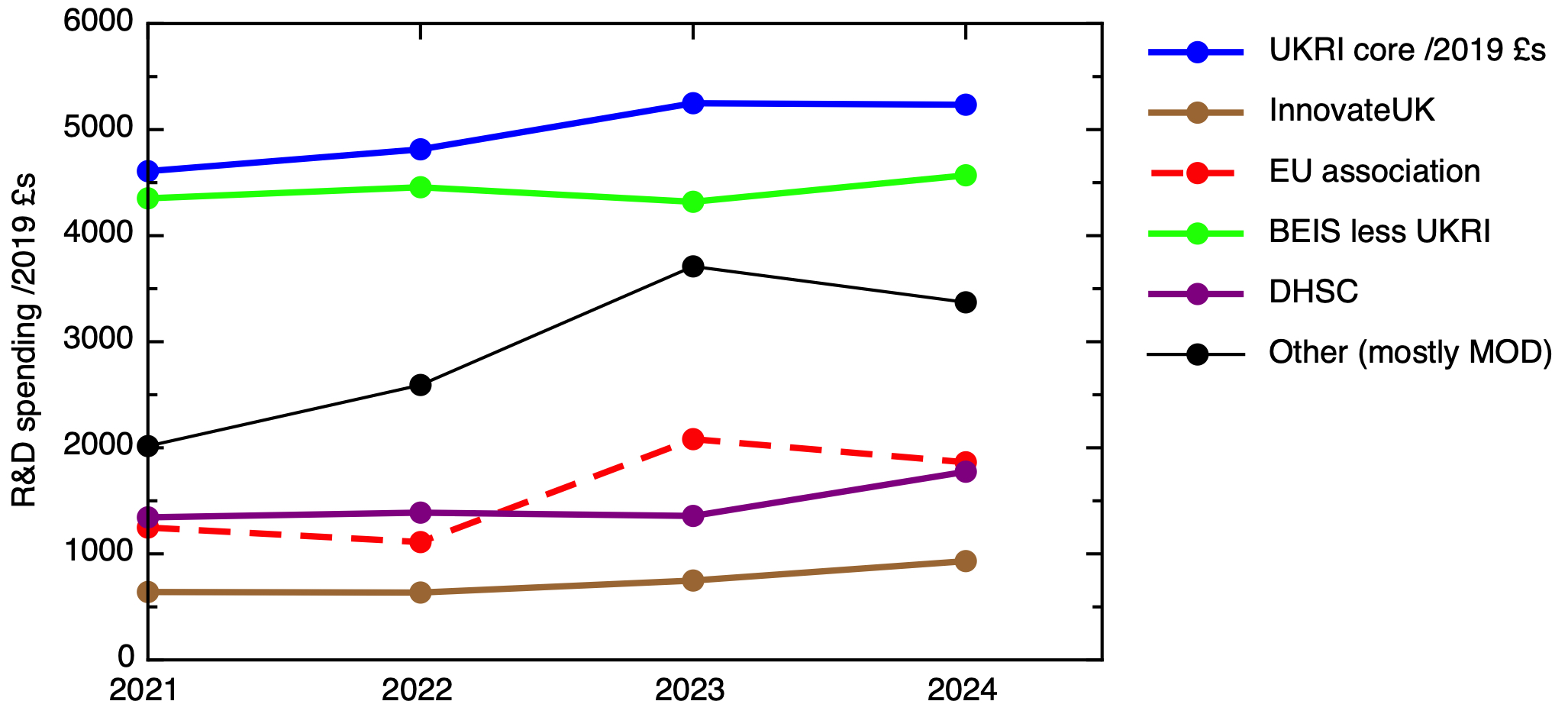

The Act of Parliament establishing ARIA does indeed give a huge amount of latitude in defining its goals and modes of operation; much is left to the discretion of the CEO and the board. The major lever the government retains is the level of funding allocated; the initial commitment is to spend £800m by 24/25. This is a relatively small amount seen in the context of the £20 billion total R&D budget planned for 24/25. Nonetheless, given that we’re already halfway through 22/23, that leaves only two years to get some entirely new programmes off the ground.

The Act does give the Secretary of State powers of Intervention on grounds of national security, and it is easy to imagine that these could be used quite widely. Nonetheless, there is some irony in the way the independence from government that was taken away from the Research Councils has been given to this new agency.

Given that the appointments of the Chief Executive and Chair have only relatively recently been announced, there is not yet clarity about what the new agency will do. I outlined my own views about how such an agency should operate in a piece from January 2020, UK ARPA: an experiment in science policy.

As I wrote then, “If we want to support visionary research, whose applications may be 10-20 years away, we should be prepared to be innovative – even experimental – in the way we fund research. And just as we need to be prepared for research not to work out as planned, we should be prepared to take some risks in the way we support it, especially if the result is less bureaucracy. There are some lessons to take from the long (and, it needs to be stressed, not always successful) history of ARPA/DARPA. To start with its operating philosophy, an agency inspired by ARPA should be built around the vision of the programme managers. But the operating philosophy needs to be underpinned by as enduring mission and clarity about who the primary beneficiaries of the research should be. And finally, there needs to be a deep understanding of how the agency fits into a wider innovation landscape.”

My starting point would be to recognise that pluralism & diversity in funding agencies is a good in itself, and we need to innovate in the way we support innovation. ARPA at its best represented an approach to funding where the focus was on the programme manager – or better, programme leader as the creative force. These leaders should be tasked with assembling and orchestrating teams of talented people to achieve ambitious programmes with concrete goals.

The archetype of the visionary leader is perhaps J.C.R. Licklider, who accepted a position with ARPA in 1962, because if offered an opportunity to realise his vision of computer networking. The research he funded at ARPA laid many of the foundations of modern computing, including the principles of networking that led to the internet, and the principles of human/computer interaction that were further developed a the XEROX PARC laboratory to give us the graphical interfaces that we all take for granted together.

ARPA benefited from a complete clarity of mission – its role was to ensure that the US armed forces enjoyed technological supremacy over any potential rival. That makes clear who its beneficiaries should be – the US Armed Forces.

What should ARIA’s mission be, and who are its beneficiaries? This remains to be decided, but from my perspective it is important to make clear that its primary beneficiaries should neither be the academic community, nor industry. Both communities will be crucial in delivering the mission, but it should not be primarily for their benefit. Instead, I believe that ARIA should focus on one, or a subset of one, of the important strategic goals that the UK state currently faces, as I outlined in the first part of this series.

For me, the most obvious candidate is the challenge of driving down the cost of achieving net zero greenhouse gas emissions to a point where the global transition can be driven by economics, rather than politics.

Up next…

In the next and final part of this series, I will attempt to sum up, with some key priorities for the UK R&D system.

Edited 20 Sept to make clear that the proposed opt-out from Pillar 3 of Horizon Europe only covers the European Innovation Council Fund. My thanks to Martin Smith for pointing this out.