What should be in the long-delayed UK Semiconductor Strategy? My previous series of three blogposts set out the global context, the UK’s position in the global semiconductor world, some thoughts on the future directions of the industry, and some of the options open to the UK. Here, in summary, is a list of actions I think the UK should – and should not – take.

1. The UK should… (& there’s no excuse not to)

The UK government has committed to spending £700m on an exascale computer. It should specify that processor design should be from a UK design house. After decades of talking about using government procurement to drive innovation, the UK government should give it a try.

Why?

The UK has real competitive strength in processor design, and this sub-sector will become more and more important. AI demands exponentially more computing power, but the end of Moore’s law limits supply of computing power from hardware improvements, so design optimisation for applications like AI becomes more important than ever.

2. The UK should… (though it probably won’t, as it would be expensive, difficult, & ideologically uncomfortable)

The UK government should buy ARM outright from its current owner, SoftBank, and float it on the London Stock Exchange, while retaining a golden share to prevent a subsequent takeover by an overseas company.

Why?

ARM is the only UK-based company with internationally significant scale & reach into global semiconductor ecosystem. It’s the sole anchor company for the UK semiconductor industry. Ownership & control matters; ARM’s current overseas ownership makes it vulnerable to takeover & expatriation.

Why not?

It would cost >£50 bn upfront. Most of this money would be recovered in a subsequent sale, and the government might even make a profit, but some money would be at risk. But it’s worth comparing this with the precedent of the post GFC bank nationalisations, at a similar scale.

3. The UK should not… (& almost certainly not possible in any case)

The UK should not attempt to create a UK based manufacturing capability in leading edge logic chips. This would need to be done by one of the 3 international companies with the necessary technical expertise – TSMC, Intel or Samsung.

Why not?

A single leading edge fab costs >£10’s billions. The UK market isn’t anywhere near big enough to be attractive by itself, and the UK isn’t in a position to compete with the USA & Europe in a $bn’s subsidy race.

Moreover, decades of neglect of semiconductor manufacturing probably means the UK doesn’t, in any case, have the skills to operate a leading edge fab.

4. The UK should not…

The UK should not attempt to create UK based manufacturing capability in legacy logic chips, which are still crucial for industrial, automotive & defence applications. The lesser technical demands of these older technologies mean this would be more feasible than manufacturing leading edge chips.

Why not?

Manufacturing legacy chips is very capital intensive, and new entrants have to compete, in a brutally cyclical world market, with existing plants whose capital costs have already been depreciated. Instead, the UK needs to work with like-minded countries (especially in Europe) to develop secure supply chains.

5. Warrants another look

The UK could secure a position in some niche areas (e.g. compound semiconductors for power electronics, photonics and optoelectronics, printable electronics). Targeted support for R&D, innovation & skills, & seed & scale-up finance could yield regionally significant economic benefits.

6. How did we end up here, and what lessons should we learn?

The UK’s limited options in this strategically important technology should make us reflect on the decisions – implicit and explicit – that led the UK to be in such a weak position.

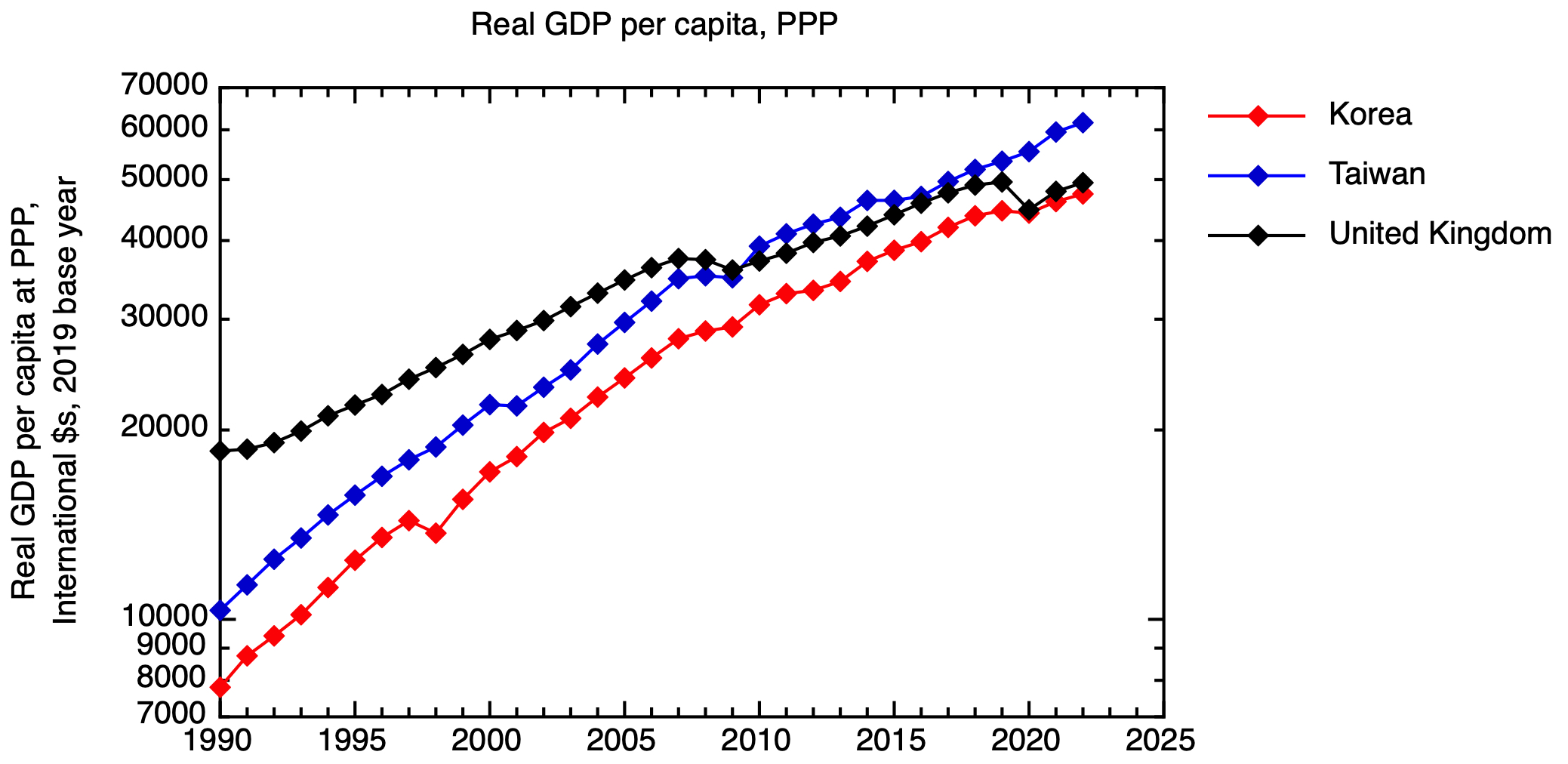

Korea & Taiwan – with less ideological aversion to industrial strategy than UK – rode the wave of the world’s fastest developing technology while the UK sat on the sidelines. Their economic performance has surpassed the UK.

Real GDP per capita at purchasing power parity for Taiwan, Korea and the UK. Based on data from the IMF. GDP at PPP in international dollars was taken for the base year of 2019, and a time series constructed using IMF real GDP growth data, & then expressed per capita.

The UK can’t afford to make the same mistakes with future technology waves. We need a properly resourced, industrial strategy applied consistently over decades, growing & supporting UK owned, controlled & domiciled innovative-intensive firms at scale.

Hi Richard,

This is your most ambition Blog Post yet!

What is your strategy regarding Industrial Policy?

I mean are there metrics or is it essentially learning

on the job?

Thank you for all the work that you do!

Zelah