I did a webinar a couple of weeks ago, for the Society of Chemical Industry, about the role of the chemicals industry in addressing the UK’s problems of stagnant productivity and regional economic disparities. The recording of the talk should be on their website soon, but in the meantime here (5 MB PDF) are the slides I used. Here’s a summary of what I said.

I started by setting out the economic context the UK finds itself in. The very slow productivity growth since the 2007/8 global financial crisis has had the result that real wages have stagnated, while economic performance across the regions of the UK remains very uneven.

The most important contributor to productivity growth – and thus to rising living standards – is what economists call “total factor productivity” – the measure of how effectively an economy converts inputs, in the form of labour and capital, into valuable outputs. This includes, but is not limited to, the technological advances that allow us to produce existing products more efficiently and to create entirely new products and services.

We can thus map the different sectors of the UK’s economy on 2 dimensions – how big a share of the economy they take, and how much their total factor productivity increases. I argue that industrial strategy should focus on those areas that are both significant in scale relative to the economy as a whole, and that are dynamic in terms of showing long-term increases in total factor productivity. The three crucial sectors in the UK economy by these measures are knowledge intensive business services, information and communication technologies, and manufacturing. Within manufacturing, transport equipment – automotive and aerospace – stand out, but chemicals and pharmaceuticals are also highly significant.

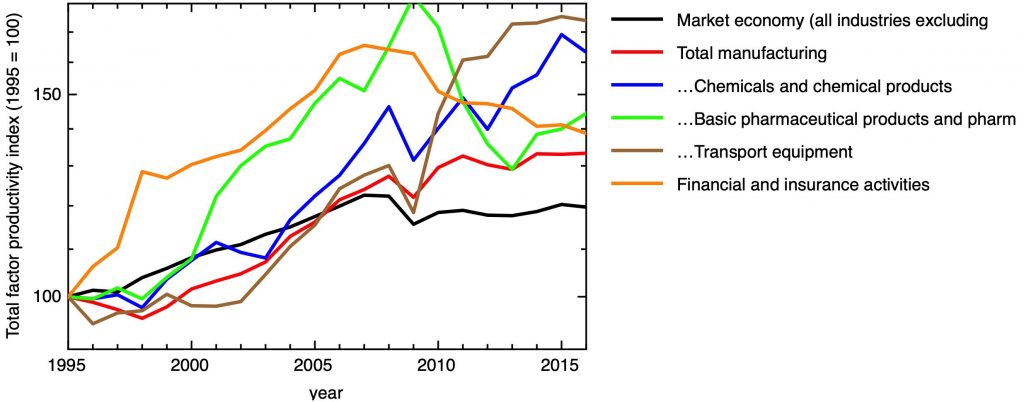

Cumulative growth in total factor productivity in selected UK sectors and sub-sectors, indexed to 1995. Data from EU KLEMS Growth and Productivity Accounts database.”

Looking at the changes in total factor productivity over the last couple of decades offers an instructive window on the way the UK’s economy has changed.

Because normally manufacturing to grows productivity faster than services, we’d usually expect total factor productivity in the manufacturing sector to grow faster than the whole market economy. In the UK, that wasn’t so in the mid-1990’s – manufacturing lagged behind the economy as a whole. But from 1998 to the global financial crisis, manufacturing TFP grew faster than the economy as a whole; since the crisis both have stagnated.

Part of the explanation for this comes from the figures for the financial services industry. This showed very fast growth in the late 1990’s, booming right up to the financial crisis – since when it has fallen precipitately. It’s at least possible that some of the apparent boom was due to the way value is measured – or mismeasured – in financial services, but it’s clear that this sector, so influential politically, has been a drag on the whole economy over the last decade.

Focusing on manufacturing subsectors, transport equipment – including automotive and aerospace – stagnated in the late 90’s, began a recovery in the 00’s, which took off dramatically after the global financial crisis. It’s intriguing that the timing of this recovery almost exactly coincides with the UK government’s rediscovery of industrial policy – with an initial focus on automotive and aerospace industries. Pharmaceutical total factor productivity boomed from the late 90’s to the end of the 00’s, then collapsing, for reasons I’ve discussed extensively elsewhere.

But the surprise – to many, I suspect – is the performance of the chemicals sector. Written off in the late 90’s as the “old economy”, the chemicals industry has delivered the steadiest gains in total factor productivity, its cumulative performance exceeding both financial services and pharmaceuticals.

What’s more, if we look at where the chemicals industry takes place, in the context of regional economic inequality and the “levelling up” agenda of the government, we find that it is located outside the prosperous southeast, in Northwest England, the Humber and Teeside.

What sectors should industrial strategy focus on? My criteria would look at relative scale, the potential to produce significant and sustained gains in total factor productivity, and to contribute to economic growth in economically lagging parts of the UK. The chemicals industry qualifies on all counts.

What, though, of the future? Economic statistics don’t capture some of the costs of the chemicals industry, but these costs are borne by society more widely. The feedstocks it uses may be unsustainable and deplete the planet’s natural capital, pollution may damage local environments and ecosystems. Improper disposal of products – like plastic packaging – at their end of life causes yet more environmental damage.

Perhaps most importantly, the energy the industry uses produces carbon dioxide and thus accelerates climate change. 3% of the UK’s greenhouse gas emissions are directly associated with the chemicals industry, which accounts for about 20% of all emissions associated with manufacturing.

There is another side of the ledger, too. The products of the chemicals industry – like batteries and fuel cells – will be crucial in decarbonising the economy. In the future we might see the widespread use of hydrogen as an energy vector, direct capture of carbon dioxide from the air, and the synthesis of hydrocarbons from green hydrogen and captured carbon dioxide for zero-carbon aviation. Much of the net zero agenda is in fact a chemical industry agenda.

We need an industrial strategy for the UK chemicals industry, justified by its scale and its record of steady total factor productivity improvement. It’s a pity that the government hasn’t responded to the Chemistry Council’s proposed Sector Deal, which would provide a good start. In addition to a focus on productivity growth, that strategy should have a regional element, building on the existing chemical industry clusters in the North West and North East with further interventions to promote innovation and skills and all levels. Above all, it should emphasise the important role and responsibility of the chemicals industry as part of the wider economic transformation that needs to take place to achieve the government’s 2050 Net Zero emissions target.