We’re in the mid-term of a government that’s placed a lot of emphasis on science and innovation for the future of the country. There’s been a lot of rhetorical ambition and some snappy slogans (“science superpower”, “innovation nation”). There’s also been a lot of change in the way the nation’s science system is wired up, and much of that change is yet to work through. In this series of four posts, I’m going to try to give an overview of where this process of change has got to and what is yet to evolve. I’ll be covering a lot of ground, so the posts will form more of an index of issues than a comprehensive discussion; each item I’ll mention will undoubtedly deserve a longer piece of its own.

Since any strategy should begin with a clear view of what one is trying to achieve, the first part of the series, below, will think about the wider challenges the UK government faces, asking what problems we need our science and innovation system to contribute to solving.

The second part will discuss some big questions about how the UK’s science and innovation system works.

- How research intensive should the UK economy be?

- Do we have the right balance between basic research and more applied development?

- Is the overall productivity of the research enterprise – in the UK and globally – growing, or falling?

- What’s the relationship of geography to innovation?

- How can national and regional economies be best equipped to take advantage of advances in science and technology made elsewhere?

The third instalment will get into the details of the UK’s R&D system as it is currently evolving, discussing what is changing, and what is yet to be resolved.

- In government support of R&D, what’s the right balance between direct commissioning and tax incentives?

- How well are the government’s agencies for supporting R&D (e.g. UK Research and Innovation, InnovateUK, the new agency ARIA, EU funding (or whatever replaces it), government departments) working, and how should they develop?

- Is the UK’s landscape of institutions where R&D is carried out optimal?

- Is the connection between policies for skills development and policies for innovation working well enough?

- How can a national government influence business R&D largely carried out by multinational companies?

- What should we make of the government’s focus on “missions” and “technologies” to organise innovation policy?

- How should the government use science and innovation policy to reduce the UK’s regional productivity disparities?

- Can the new National Science & Technology Council effectively develop national strategy for science and innovation, and convert that into implementable policy across the whole of government?

Finally, I’ll sum up by asking what it might mean for the UK to be a “science superpower”. Given the UK’s current position in the world as a medium size economy, accounting for about 2-3% of the worlds added value from knowledge & technology intensive industries, what is a realistic aspiration for the UK’s science and innovation system?

With that introduction, on to part 1 of this series of blogposts.

1. What problem(s) are we trying to solve?

1.1. Getting the UK economy growing again

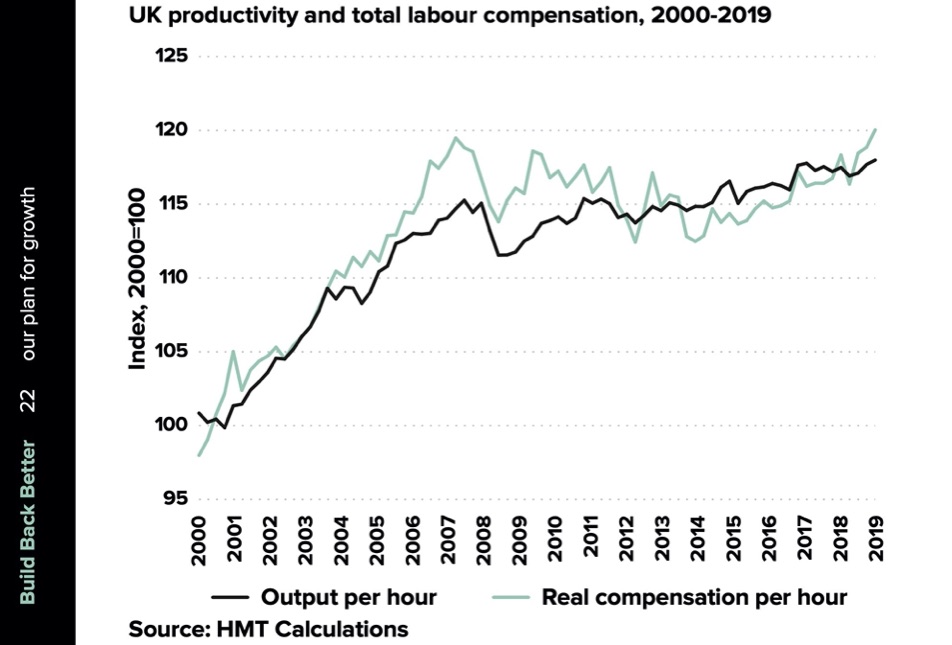

The UK’s most serious economic problem now is its lack of productivity growth. As I’ve discussed many times here, after many decades in which productivity grew at a steady rate, a little more than 2% a year, this growth was arrested after the global financial crisis in 2008; since then productivity has been more or less stagnant. This translates directly into a stagnation in average wages, as the first plot shows – this is the painful backdrop to the current “cost of living crisis”.

Productivity and average wages since 2000. From Build Back Better: our plan for growth, HMT, March 2021

This stagnation almost certainly has more than one cause. There may be some general factors affecting all developed economies. Progress in some areas of technology may be slowing; the exponential growth in computer power that came from the combination of Moore’s law and Dennard scaling came to an end in the mid-2000s, for example. But, while productivity growth in all developed countries has slowed, the stagnation has been more pronounced in the UK than any other advanced economy except Italy.

Structural effects specific to the UK include the rapid fall-off of North Sea oil and gas production since the early 2000s, and the unwinding of the bubble in financial services that burst in the global financial crisis. The combination of North Sea oil and the financial services boom may have led to a touch of “Dutch disease”, squeezing other sectors such as manufacturing. There have been difficulties in specific sectors that the UK has been specialised in – notably pharmaceuticals.

There’s an effect of some policy choices over the last decade; macroeconomists focus on the role of demand in driving productivity growth, so the effects of the fiscal consolidation of the early 2010s may themselves have contributed. Other economists highlight the beneficial role of international trade in driving productivity growth, so the choice to impose additional frictions on international trade will give an additional headwind over coming years.

But the fundamental driver of productivity growth is innovation, which finds ways of reducing the inputs needed to produced existing goods and services, and develops entirely new, highly valued goods and services. Not all innovation arises from formal research and development, but it is striking that the UK’s decline in productivity growth follows a period in which the overall R&D intensity of the UK economy declined substantially, and that the UK’s weak performance in productivity growth compared to international comparator countries is correlated with comparatively low R&D intensity.

In terms of productivity, the UK is a highly divided country. The Greater Southeast – London, the Southeast, parts of East Anglia – has an economy with a comparable level of productivity to other high performing Northern European economies, but most of the rest of the country more closely resembles Southern Italy, Spain or Portugal. Moreover, the UK’s large second tier cities – Birmingham, Manchester, Glasgow etc – instead of being drivers of the national economy, actually have levels of productivity below the national average.

Without a recovery of productivity growth, wages will continue to stagnate, living standards will fall, and it will be impossible for governments to provide public services of a quality that people have come to expect. It will not be possible for one corner of the nation to carry the economy of the whole country, so it should be a priority to raise the productivity of those parts that are currently lagging behind their potential – particularly the UK’s large, second tier cities. This is the pre-eminent economic driver that the development of science and innovation policy needs to focus on.

1.2. Managing the energy transition to net zero

All western economies and lifestyles depend on the availability of cheap, abundant energy – and this has been supplied by fossil fuels, which still account for around 80% of our energy supplies. But our dependence on fossil fuels has driven accelerating and potentially disruptive climate change. There’s widespread agreement about the need for our energy system to make a transition to one that stabilises the output of greenhouse gases, and in the UK a commitment to producing net zero greenhouse gases by 2050 is rightly enshrined in legislation. But it isn’t clear to me that policy makers and politicians fully understand the scale of this challenge.

The UK has made some good progress in decarbonising its energy economy, but naturally the UK has done the easy bits first. We’ve exported much of our heavy industry, shifted electricity generation from coal to gas, and we now get roughly half of our electricity generation from a combination of burning biomass, offshore wind and the continuing operation of legacy nuclear power stations.

What remains will be much more difficult. The majority of our energy use still comes from directly burning oil and gas, for transport and domestic and industrial heat. We need to reduce demand by much more focus on energy efficiency, especially in heating. This will need a major drive to retrofit existing commercial and residential buildings, and a large scale programme building out new, zero-carbon social housing, with the remaining heating needs being met by electric heat pumps

The transition to electric vehicles needs to accelerate; heavy goods vehicles and shipping may need to transition to hydrogen or ammonia, while in my view long-haul aviation will only be viable powered by synthetic, zero carbon hydrocarbons (e-fuels). These new fuels themselves need to be synthesised in a zero carbon way – hydrogen by electrolysis using renewable energy and/or high temperature process heat from high temperature nuclear reactors, synthetic hydrocarbons from green hydrogen and carbon dioxide captured directly from the atmosphere.

In addition to being totally decarbonising our electricity supply, we’ll need to substantially expand it to accommodate this transition from directly burnt oil and gas to electricity. The heavy lifting in the UK will likely be done by offshore wind, including floating offshore wind. In addition to intermittent renewables, we’ll need both more storage capacity, and sources of zero carbon firm power. For the latter, the choice is between continuing to burn gas, but with carbon capture and storage, and a bigger programme of nuclear new build. For why I think the latter route is both preferable and more likely, see my earlier post: Carbon Capture and Storage: technically possible, but politically and economically a bad idea. We should support fusion R&D (where the UK has a genuine comparative advantage) in case it works, though it isn’t likely, in my view, to make a substantial contribution to the 2050 net zero target.

This is a daunting list, combining some established technologies, some that exist but aren’t yet cheap or deployable at scale enough, some that exist only in principle. The scale of the transition is wrenching, and like all big changes, it will produce winners and losers, both at a national level and geopolitically. We need innovation to drive down the cost of the new, cleaner technologies to the point at which economic forces drive the transition more than political ones.

1.3. Keeping the nation secure in a more dangerous world

We now have a full-scale European war involving a nuclear-armed adversary, reminding us forcefully that one of the primary duties of a state is to keep its people secure. The 2021 Integrated Review of Security, Defence, Development and Foreign Policy reasserted the importance of science and technology as a source of strategic advantage and as a central part of national security. Although the war in Ukraine has called into question some of the assumptions of the Integrated Review, with a painful reminder that the security of our European neighbourhood can’t be taken for granted, this emphasis on security as a key motivation for the state’s involvement in science and technology will surely only strengthen.

The Ukraine war has also reminded us that the geopolitics of energy never went away, and that the resilience of the material base of the economy and our lives can’t be taken for granted. Since the end of the Cold War and the subsequent deepening of globalisation, we have become complacent about the degree of our dependence, as a small country, on imports for energy, food, materials and finished goods. Of course, our prosperity depends greatly on our international trade, so a North Korea-style Juche-UK policy would be ridiculous – but the pandemic reminded us of our dependence on other countries for some essential items like PPE and pharmaceutical precursors, as well as teaching us how sensitive our complex global supply chains have become, with the effects of disruptions in obscure corners rippling out worldwide.

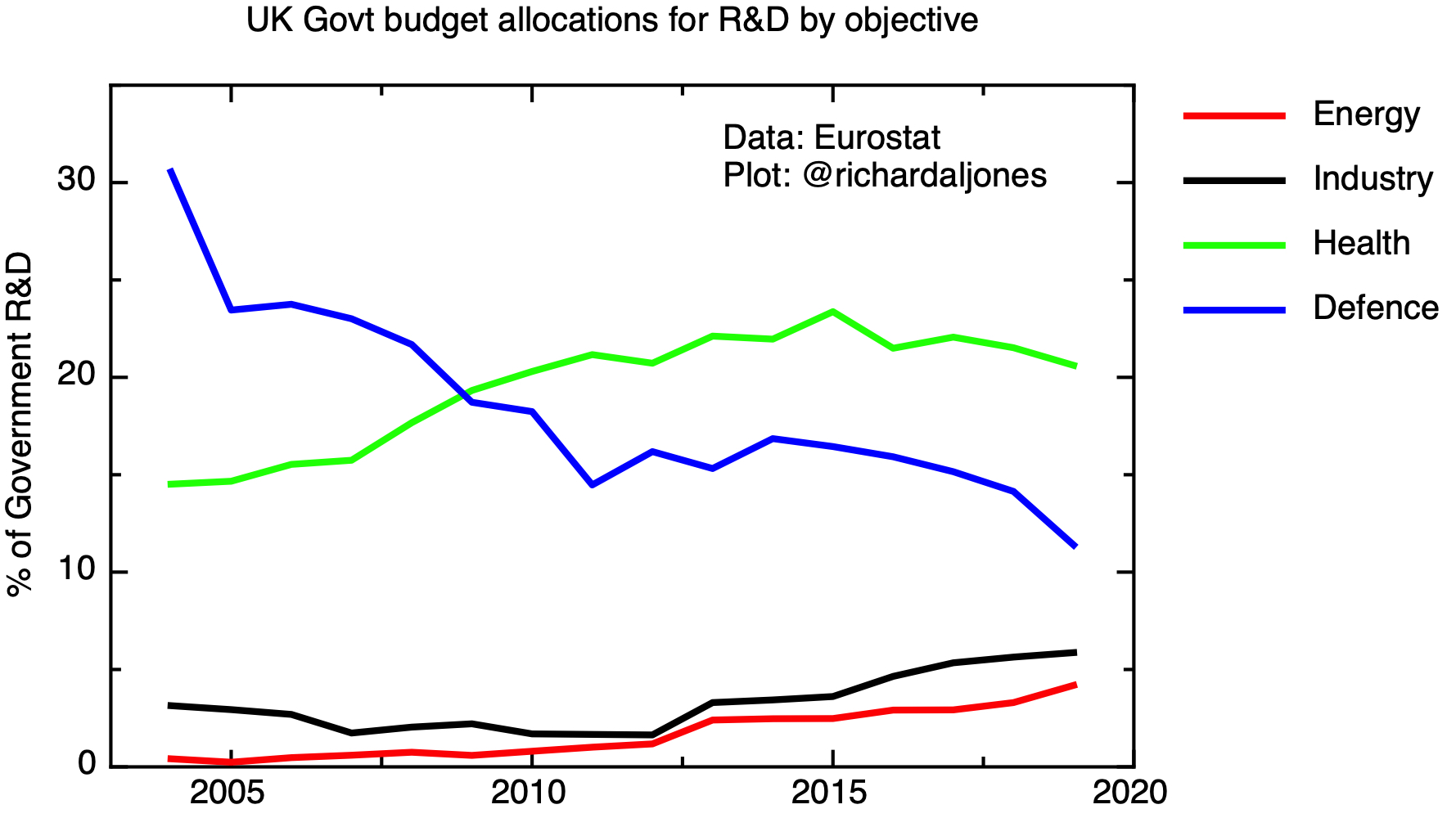

UK government research and development spending by socio-economic objective, for selected sectors. Data: Eurostat (GBARD)

After the end of the Cold War, one of the ways in which we cashed in the “peace dividend” was by reducing the amount of R&D devoted to defense, as my last post discussed in more detail. We’re in a different world now, so, as I wrote there, priorities for the government’s R&D spending will inevitably and rightly be different, with more emphasis on food and energy security, rebuilding sovereign capabilities in some areas of manufacturing; as well as a return to higher spending directly on defence R&D, including new threats to cybersecurity.

1.4. Keeping an ageing population healthy

The pandemic has been a traumatic experience for the nation, with more than 175,000 deaths to date. As the UK went into the pandemic, there was some optimism that its strong position in life sciences would place it in a better position to weather the pandemic than other countries. As it turned out, its record was mixed. On the one hand, there was a successful rapid vaccination programme; on the other, the pandemic was unforgiving in the way it revealed and exacerbated widespread health inequalities.

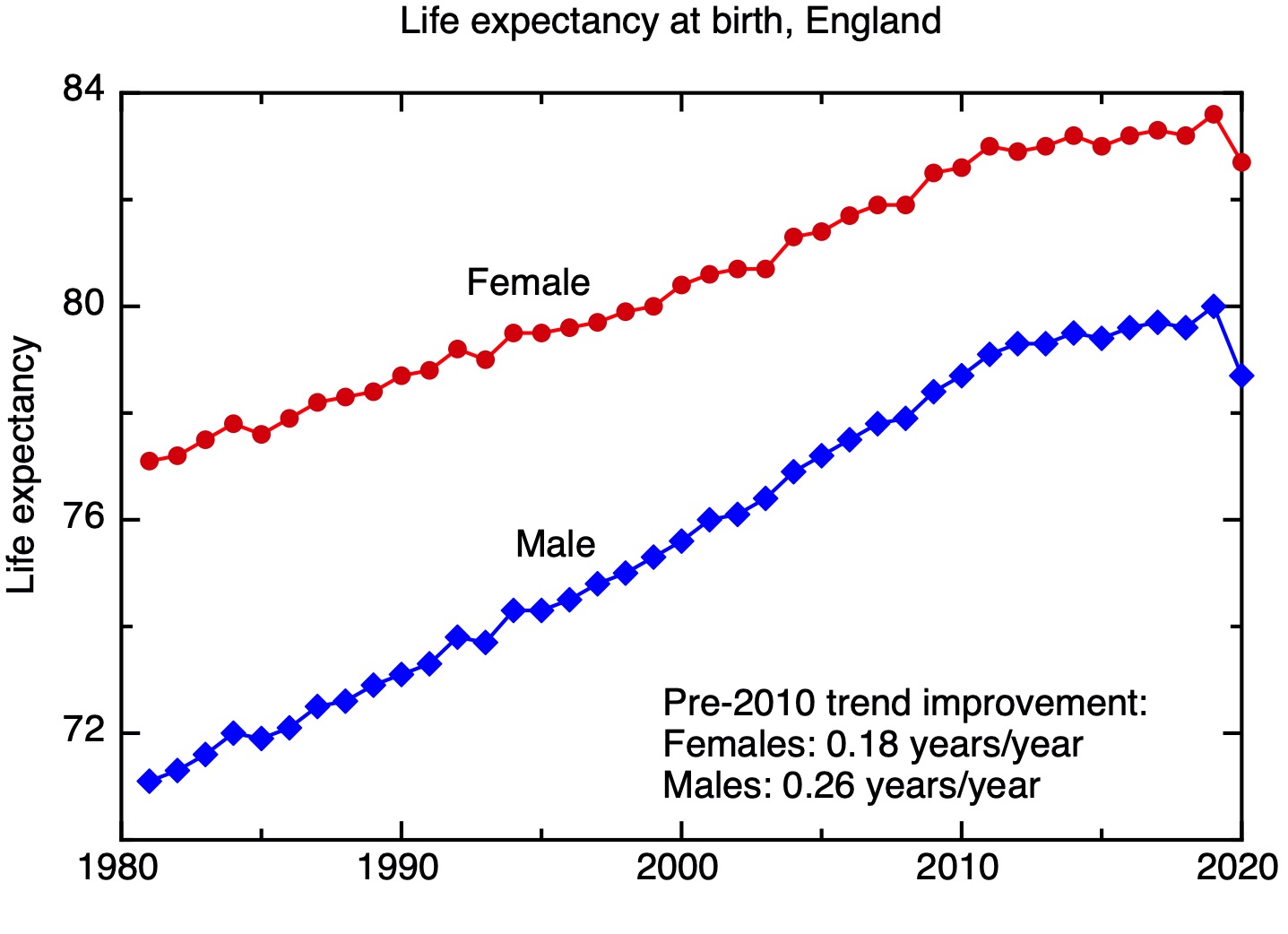

Life expectancies at birth for males and females in 2020 for England. These are not predictions of how long a baby born in 2020 will live; instead they represent an estimate of the average number of years a baby born in 2020 would live if they experienced the age-specific mortality rates for 2020 throughout their life. Data from Public Health England.

A more complete reckoning of the strengths and weaknesses of the UK’s pandemic response awaits a full inquiry. The plot shows the impact of the pandemic on life expectancies. What is interesting, though concerning, is that even before the pandemic the rate of increase in life expectancies that we’d seen in 1980’s, 90’s and 2000’s had already, after 2010, begun to stall.

The paradox here is that this slow-down in the rate of improvement of life expectancy follows soon after the substantial increase in R&D devoted to health. As always, there are probably many factors at play here. But there is a conceptual muddle, in my view, about the way the UK thinks about its “Life Sciences Strategy”. The problem is that this strategy has two, largely separate, goals, which are sometimes in tension.

One objective of a life sciences strategy is to do the research needed to improve the way healthcare is delivered to the UK’s population, and to address the broader determinants of the health of the public. The other is to support the UK’s pharmaceutical and biotechnology industries. These are important areas of comparative advantage for the UK economy, strong exporting sectors. But in recent years, as I’ve already mentioned, productivity growth in the pharmaceutical sector has markedly slowed down, and given the UK’s specialisation in pharma, this underperformance has made a material contribution to the UK’s overall productivity problem, as demonstrated by this recent research.

So while it is an entirely appropriate piece of industrial strategy to support the pharmaceutical and biotechnology sectors, it’s important also to think about the wider innovation needs of the health and social care system. Nor should we expect the pandemic we have just been through to be the last, so we should pay some attention to making sure we’re better prepared for the next one.

As other priorities for R&D – like national security and net zero – become more pressing, it is going to be more important than ever to be clear about how we set our strategic priorities.

To come next: part 2 – Some overarching questions about the UK’s research & innovation system.